Executive Summary

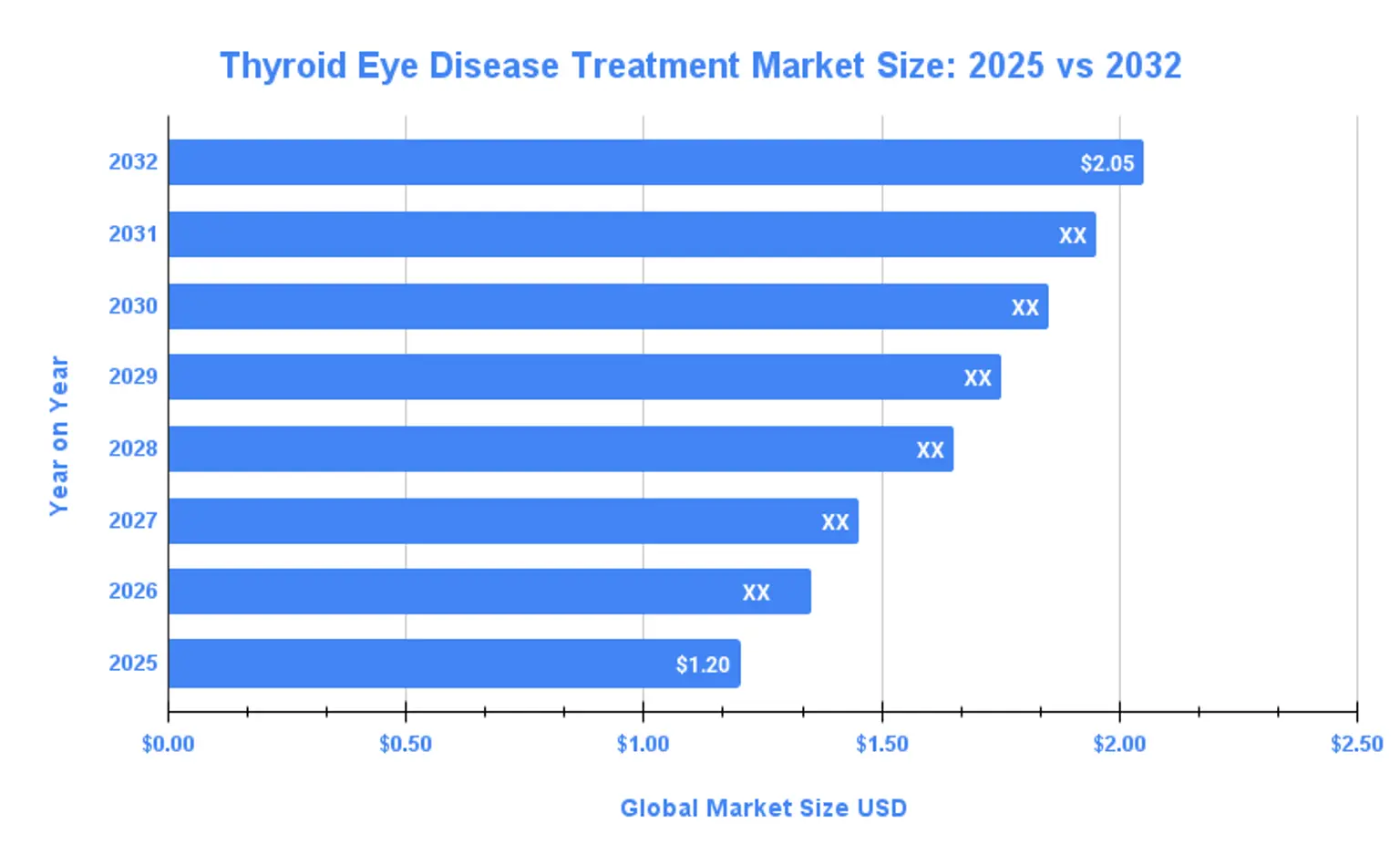

executive-summaryThe global thyroid eye disease (TED) treatment market is projected to grow steadily between 2025 and 2032. The market is valued at USD 1.2 billion in 2025 and is expected to reach USD 2.05 billion by 2032, expanding at a CAGR of 8.1%.

Growth is driven by improved diagnosis, rising awareness of autoimmune thyroid conditions, and the introduction of biologic therapies that directly target disease pathways. Biologics and monoclonal antibodies lead treatment type share. Hospitals remain the largest end users. North America dominates global revenue, while Asia Pacific shows the fastest growth rate.

For international patients, these trends reflect expanding access to targeted treatments and improved disease management options.

Global Market Size Comparison: 2025 vs 2032

global-market-size-comparison-2025-vs-2032The market nearly doubles between 2025 and 2032.

Thyroid Eye Disease Treatment Market Size

thyroid-eye-disease-treatment-market-size

The increase from USD 1.2 billion to USD 2.05 billion reflects sustained demand for advanced TED therapies. Why this matters to patients: growing investment in this condition improves treatment availability and innovation.

Market Growth Trend

market-growth-trendThis shows a steady upward expansion over the forecast period. Why this matters to patients: consistent growth often supports broader insurance coverage and treatment access.

CAGR

cagrThe market is expanding at a compound annual growth rate of 8.1% from 2025 to 2032.

Understanding Thyroid Eye Disease Treatment

understanding-thyroid-eye-disease-treatmentThyroid eye disease is linked to autoimmune thyroid disorders, particularly Graves’ disease. It can cause:

- Eye inflammation

- Tissue swelling

- Proptosis (eye bulging)

- Visual impairment

Treatment options include:

- Corticosteroids

- Immunomodulatory drugs

- Biologic therapies

- Radiation therapy

- Surgical interventions such as orbital decompression

New biologic drugs specifically target immune pathways that drive inflammation and tissue expansion.

Product differentiation focuses on:

- Symptom reduction

- Safety profile

- Treatment duration

- Improvement in quality of life

Market Segmentation Analysis

market-segmentation-analysisBy Treatment Type

by-treatment-typeBiologics and monoclonal antibodies hold 45% market share, making them the dominant treatment type. This segment is also the fastest growing.

Reasons for dominance:

- Targeted mechanism of action

- Improved safety profile

- Reduced disease progression

Corticosteroids remain important for symptom control but carry relapse risk and side effects. Surgical interventions are mainly used in severe or refractory cases. Radiation therapy is used selectively due to safer alternatives.

Why this matters to patients: targeted biologics are increasingly becoming first-line options for eligible patients.

By Therapeutic Approach

by-therapeutic-approachImmunomodulatory therapy accounts for over 50% of market share. It is also the fastest-growing therapeutic approach.

This category includes biologics that directly modulate immune responses involved in TED.

Other approaches include:

- Symptomatic management

- Surgical procedures

- Radiotherapy

- Supplementary treatments such as lubricants and antioxidants

Surgery is critical for optic neuropathy or severe proptosis but is less frequent due to invasiveness.

Why this matters to patients: immune-targeted therapies now play a central role in managing disease progression.

By End User

by-end-userHospitals hold close to 60% of the market share.

Reasons hospitals dominate:

- Complex diagnostics capability

- Multidisciplinary care

- Postoperative management

- Clinical trial participation

Specialty clinics are the fastest-growing subsegment due to:

- Personalized care

- Outpatient management pathways

Ambulatory surgical centers mainly support surgical cases. Research institutes influence treatment development but hold smaller direct market share.

Why this matters to patients: hospital settings remain central for complex or advanced TED management.

Regional Market Insights

regional-market-insightsNorth America

north-americaNorth America holds approximately 40% global market share in 2025.

Growth drivers include:

- Advanced healthcare infrastructure

- High healthcare expenditure

- Strong reimbursement systems

- High disease prevalence

The United States generates around 40% of global TED treatment revenue. Teprotumumab prescriptions grew by over 50% year-over-year in 2024 in the U.S. Global prescriptions for teprotumumab increased by over 35% in 2024.

Why this matters to patients: strong insurance coverage and biologic availability support treatment access.

Asia Pacific

asia-pacificAsia Pacific is the fastest-growing region, with a CAGR exceeding 10%.

Drivers include:

- Rising disease awareness

- Expanding hospital infrastructure

- Increasing adoption of new treatment modalities

- Government initiatives to improve specialty care access

Countries such as India and China report rising diagnosis rates due to awareness campaigns.

Why this matters to patients: treatment accessibility is expanding rapidly in this region.

Market Trends and Technological Integration

market-trends-and-technological-integrationShift Toward Biologics

shift-toward-biologicsRecent FDA approval and adoption of teprotumumab significantly transformed treatment outcomes.

Combination therapies using corticosteroids and biologics are increasing. Clinical trial registrations for combination protocols rose by 18% globally in 2024.

Manufacturing capacity for immunomodulatory agents increased by approximately 22% between 2023 and 2025.

Why this matters to patients: expanded manufacturing supports steady drug supply and reduced shortages.

Digital Health and Teleophthalmology

digital-health-and-teleophthalmologyTelemedicine consultations related to TED management increased by 18% year-over-year in 2024.

Digital tools support:

- Disease monitoring

- Treatment adherence

- Remote specialist consultations

Why this matters to patients: remote care improves follow-up access, especially for international patients.

Growth Drivers

growth-driversKey growth drivers include:

- Improved disease diagnosis

- Introduction of biologic treatments

- Rising prevalence of Graves’ disease (12 million Americans affected as of 2024)

- Expanding ophthalmic specialty care centers

- Improved reimbursement policies

These factors collectively strengthen early intervention and access to advanced therapies.

Market Developments

market-developmentsRecent developments include:

- Submission of a Biologics License Application for Veligrotug in 2024

- Royalty agreements expanding exposure to U.S. TED therapies

- 30% revenue growth in 2024 from successful biologic commercialization

- Strategic licensing and collaboration expansion in emerging markets

These moves reinforce biologics-focused competition.

Historical Evolution of TED Treatment

historical-evolution-of-ted-treatmentEarlier TED management relied heavily on corticosteroids and surgery. Advances in understanding autoimmune mechanisms enabled the development of targeted biologic therapies. These innovations significantly improved long-term disease control and reduced progression rates.

Leading Companies

leading-companiesKey companies include:

- Santen Pharmaceutical Co., Ltd.

- Sanofi S.A.

- AbbVie Inc.

- Regeneron Pharmaceuticals, Inc.

- Alexion Pharmaceuticals, Inc.

- Eisai Co., Ltd.

- Amgen Inc.

- Mylan N.V.

- Ipsen S.A.

- Ipsen Bioscience, Inc.

Market leaders are expanding biologics portfolios and strengthening global distribution strategies.

Future Outlook

future-outlookThe market is expected to grow as:

- Early diagnosis increases

- Biologic therapies continue evolving

- Multidisciplinary care expands

- Emerging markets improve specialty access

Improved healthcare infrastructure will support broader treatment adoption globally.

FAQs

faqsQ1: What is the projected market size of thyroid eye disease treatment by 2032? A1: The market is expected to reach USD 2.05 billion by 2032, growing at a CAGR of 8.1% from 2025.

Q2: Which treatment type dominates the TED market? A2: Biologics and monoclonal antibodies lead with 45% market share and are the fastest-growing segment.

Q3: Which region holds the largest market share? A3: North America accounts for approximately 40% of global market share in 2025.

Q4: Why are hospitals the leading end users? A4: Hospitals provide complex diagnostics, multidisciplinary care, and postoperative management, holding close to 60% share.

Q5: How is Asia Pacific performing in this market? A5: Asia Pacific is the fastest-growing region, with a CAGR exceeding 10%, driven by rising awareness and expanding healthcare access.